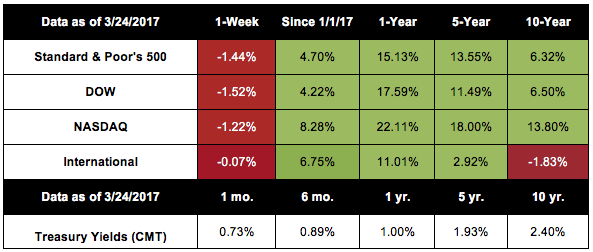

Last week, all four of the indexes we discuss in these market updates saw their performance stumble. The S&P 500 lost 1.44%, the Dow was down 1.52%, the NASDAQ gave back 1.22%, and the MSCI EAFE declined 0.07%.

On Tuesday, March 21, the S&P 500 and Dow recorded 1% declines for the first time since Oct. 11, 2016. By Friday, the S&P had posted its worst week since the election. At the same time, 10-year Treasury yields fell and the dollar dropped for the second straight week.

What happened? As is typically the case, no simple answer can easily explain market behavior. Last week’s health care headlines — and the House of Representatives’ decision not to vote on the American Health Care Act of 2017 — may have caught the attention of many people on Wall Street. As a result, pundits will likely spend significant time debating what lies ahead for health care, tax reform, and other governmental policies. We again encourage you to look at the economic fundamentals rather than allowing news coverage to determine your financial confidence.

Recent Economic News

We did not receive a tremendous amount of new data between March 20 and 24, but three new reports did stand out: durable goods, new single-family home sales and existing home sales.

Durable goods orders increased 1.7%. Orders for durable goods (items expected to last) beat expectations in February and are up 5% since this time last year. While commercial aircraft orders accounted for a significant portion of the increase, data throughout the report may indicate that business investment and confidence is on the rise.

New single-family home sales increased 6.1%. In February, sales of new single-family homes hit their second-fastest growth since 2008. Even as home prices and mortgage rates rise, demand for new homes has grown by 12.8% in the past 12 months.

Existing home sales dropped 3.7%. Coming off January, where we saw the fastest pace of existing home sales since 2007, the report missed expectations in February. Low inventory of available houses is pushing prices higher and may be keeping some potential buyers from moving forward. In the past year, median prices have risen 7.7%; meanwhile, sales are 5.4% higher.

This week, we will receive the Q4 GDP final reading, as well as insight into personal income, consumer sentiment, and consumer confidence. This and other forthcoming data provides the foundation necessary for clearly understanding the economic environment.

We understand how compelling the news and political conversations can be, and there is no denying that policies can affect the economy. However, we are here to help you gain the perspectives you need to know where you stand in your unique financial life — rather than what the headlines may urge you to believe.

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance, S&P Dow Jones Indices and Treasury.gov. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.